Resident (of India) Definition:

An individual will be classified as a Non-Resident for the previous year if they do not meet both of the following criteria:

- If they stay in India for 120 days instead of the usual 182 days.

- Alternatively, if they spend 60 days or more in India during the previous year and a total of 365 days or more in the four years leading up to that previous year.

Taxes for non-resident Indians in India:

According to the new regulation, a non-resident Indian who resides in India for more than 120 days and earns 15 lakhs from Indian sources (excluding foreign income) will be required to pay taxes similar to those of a resident Indian, provided they are not subject to tax in any other country.

Additionally, for Indian citizens and persons of Indian origin visiting India within the year, the 60-day period mentioned above will be replaced with 182 days. A similar provision applies to Indian citizens who leave India in any previous year as crew members or for employment purposes abroad.

Taxes on Global Income for non-resident Indians:

As per NRI Taxation Under New Regulations, non-resident Indians (NRIs) will be subject to taxation. If you qualify as a “resident but not ordinary resident” (RNOR), your income—whether active or passive—earned outside of India may be taxable. This includes interest from bank accounts, dividends from foreign stocks, and capital gains from the sale of overseas assets.

New Rules for Liberalized Remittance Scheme

- Indian residents remitting more than 7 lakhs abroad may face the potential higher taxes on the source income.

- Remittances for education and medical treatment will undergo scrutiny and require detailed documentation.

Mandatory disclosures for non-resident Indians:

All non-resident Indians, including OCI cardholders (NRIs and OCI card holders), are required to disclose their assets located outside of India. This encompasses various holdings such as bank accounts, stocks, cryptocurrencies, real estate, and other assets. Along with reporting their investments and bank accounts, non-resident Indians must also declare the taxes they have filed, including any tax refunds and rebates, in their country (or countries) of residence. Stricter regulations will apply for the declaration of “Double Tax Avoidance Agreement (DTAA).” The Income Tax department may request more documentations.

- Assets including bank accounts and deposits, stocks (located outside India), cryptocurrency, real estate, and other forms of assets.

- Capital gains from mutual funds, ETFs, REITs, and similar investments.

- Foreign pensions and retirement accounts, such as 401(k) in the USA, Japan’s iDeCo pension system, the UK workplace pension, Mandatory Provident Fund in Hong Kong, EPF in the UAE, and Superannuation in Australia, etc. along with their withdrawal details.

Please be aware that Indian authorities will actively monitor and investigate your foreign assets and income, if applicable.

Penalty for hiding or incomplete disclosures:

Not disclosing these assets or failing to report complete or correct documents could result in penalties, which may additional include criminal prosecution.

- A tax of up to 300% may be imposed on those assets, along with the risk of criminal prosecution.

- Individuals found guilty could face charges under anti-money laundering legislation.

- There is a potential for income to be seized if it exceeds 50 lakh and is located outside of India.

How to disclose your income and assets?

Income Tax Department (It can be accessed after logging on to Income Tax e-Filing portal)

Go to e-filing portal > login > AIS

Details provided in the form:

- Tax Deducted / Collected at Source

- SFT Information

- Payment of taxes

- Demand / Refund

Other information (like Pending/Completed proceedings, GST Information, Information received from foreign government etc)

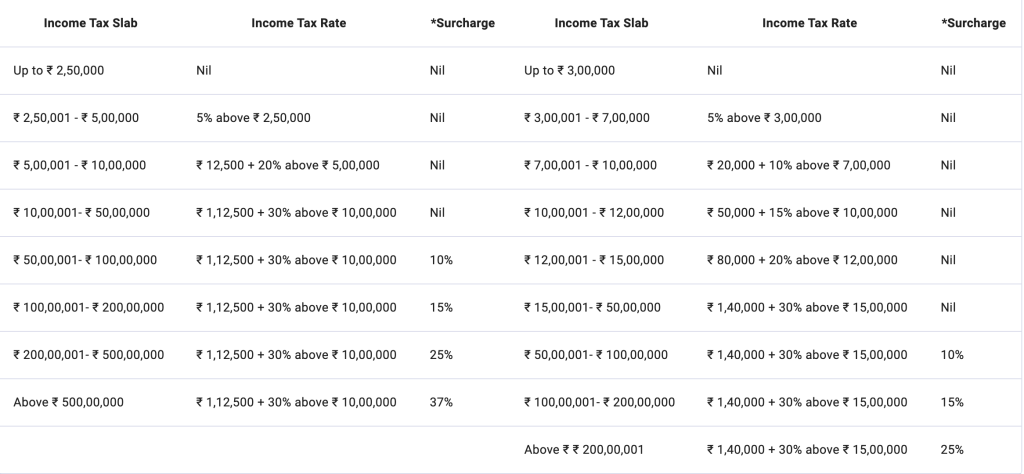

Tax rates for Non Resident Individual as per new Income Tax Rule 2025:

(Source: Income Tax Department Official Website)

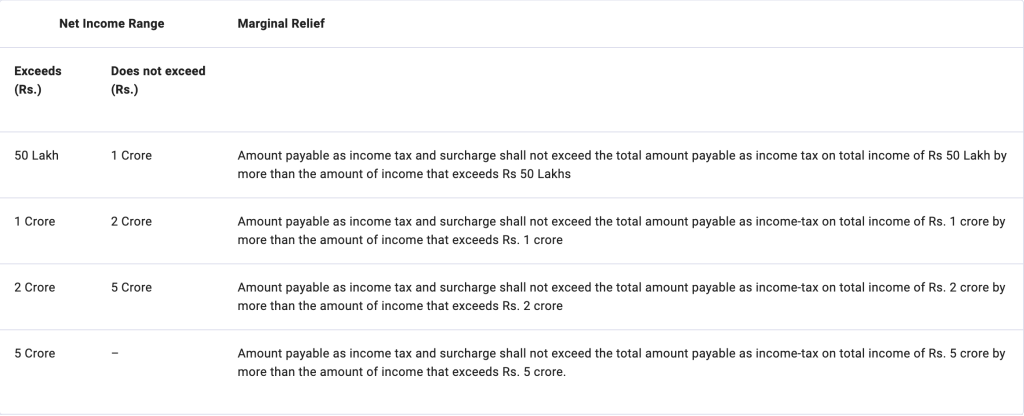

Marginal relief can be claimed from surcharge if the amount of income earned exceeding ₹ 50 lakhs, ₹ 1 crore, ₹ 2 crore or ₹ 5 crores respectively as under:

ITR 2

This return is applicable for Individual (whether Resident or Non-Resident) and Hindu Undivided Family (HUF).

ITR3

This return is applicable for Individual (whether Resident or Non-Resident) and Hindu Undivided Family (HUF).

Taxes for Foreign Business Owners

Foreign companies serving Indian clients will be required to pay taxes on their profits. According to the new Significant Economic Presence (SEP) Rule, any business, regardless of whether it has a physical office in India, may be subject to taxation if it provides services to Indian clients. This applies to multinational firms, including IT companies, consultants, e-commerce platforms, and those in the service industry that sell their products or services in the Indian market.

Please consult your chartered accountant in India or visit Income Tax Official website for more details.

{kind=link}